KUALA LUMPUR (April 5): The average government debt level in the Asia-Pacific region — which is at an 18-year high — is not necessarily bad news, according to the United Nations (UN) Economic and Social Commission for Asia and the Pacific (Escap) through its Economic and Social Survey of Asia and the Pacific 2023.

The survey, titled “Rethinking Public Debt for the Sustainable Development Goals (SDGs)”, argued that current policy debates around public debt sustainability do not sufficiently account for the long-term positive socio-economic and environmental impact of public investments.

It said that this type of spending lays sound foundations for inclusive, resilient and sustainable prosperity.

“A higher debt level does not necessarily mean a higher risk of debt distress. Nor is higher debt necessarily detrimental to economic growth.

“Rather, deploying public debt as an investment in people and the planet offers sizeable medium- and long-term economic, social and environmental returns,” Escap under-secretary general and executive secretary Armida Salsiah Alisjahbana said.

Notably, the current high levels of government debt are largely a result of the unprecedented expenditure to cope with the Covid-19 pandemic and the resulting economic contraction.

“Public debt distress is expected to worsen amid the global economic slowdown, record high inflation and rising interest rates, and uncertainty induced by the war in Ukraine.

“This implies that the scale of fiscal responses available for investing in the SDGs and for climate action is likely to remain limited,” she said.

Thus, a reconsideration of the public debt development nexus is required to effectively pursue sustainable development under difficult economic conditions.

The survey also argued for international financial institutions and credit rating agencies to consider the positive long-term economic, social and environmental (ESG) outcomes of investing in the SDGs in their assessments of public debt sustainability, while considering whether such spending would boost economic productivity.

“Debt relief should be viewed as helping to support the fiscal outlook, rather than as a sign of an upcoming debt default.

“At the same time, countries with high debt distress levels may need pre-emptive, swift and adequate sovereign debt restructuring, while efforts towards common international debt resolution mechanisms and restructuring frameworks also need to be accelerated,” she said.

Additionally, effective public debt management reduces fiscal risks and borrowing costs, as there are several examples of good public debt management practices in the Asia-Pacific region.

Produced annually since 1947, the survey is the oldest UN report on the region’s development progress, which provides analyses to guide policy discussions on current and emerging socio-economic issues and policy challenges to support inclusive and sustainable development in the Asia-Pacific region.

Debt securities most prevalent instrument for countries with higher domestic debt

Asean countries have successfully grown their domestic debt securities market since the 1997 Asian financial crisis, according to the report.

Loans and other accounts payable are the two other common instruments of domestic debt. Debt securities include such securities as treasury bills, bonds, and some other securities that are unique to each country.

Debt securities account for more than 90% of total domestic government debt in Indonesia, Malaysia, the Philippines and Thailand, it noted.

Meanwhile, foreign holdings of local currency (LCY) government bonds have been on an upward trend generally after 2008, but have also experienced fluctuations over the years, according to the report.

Citing external research, it said foreign investors’ participation in the LCY government bond market can generate significant benefits, such as greater diversity of investors, a broader investor base, as well as greater depth and liquidity for the domestic debt market.

The enhanced liquidity and additional demand could also help to reduce borrowing costs.

“However, greater participation of non-residents in government bond markets also means an increase in the risk exposure to government bonds held by financial companies, which include pension funds and insurance companies,” said the report.

Specifically, until 2020, Indonesia had seen the highest foreign participation in the LCY government bond market. Malaysia now has the highest holdings of LCY government bonds by foreign investors, according to Asian Bonds Online, despite a declining trend since 2016.

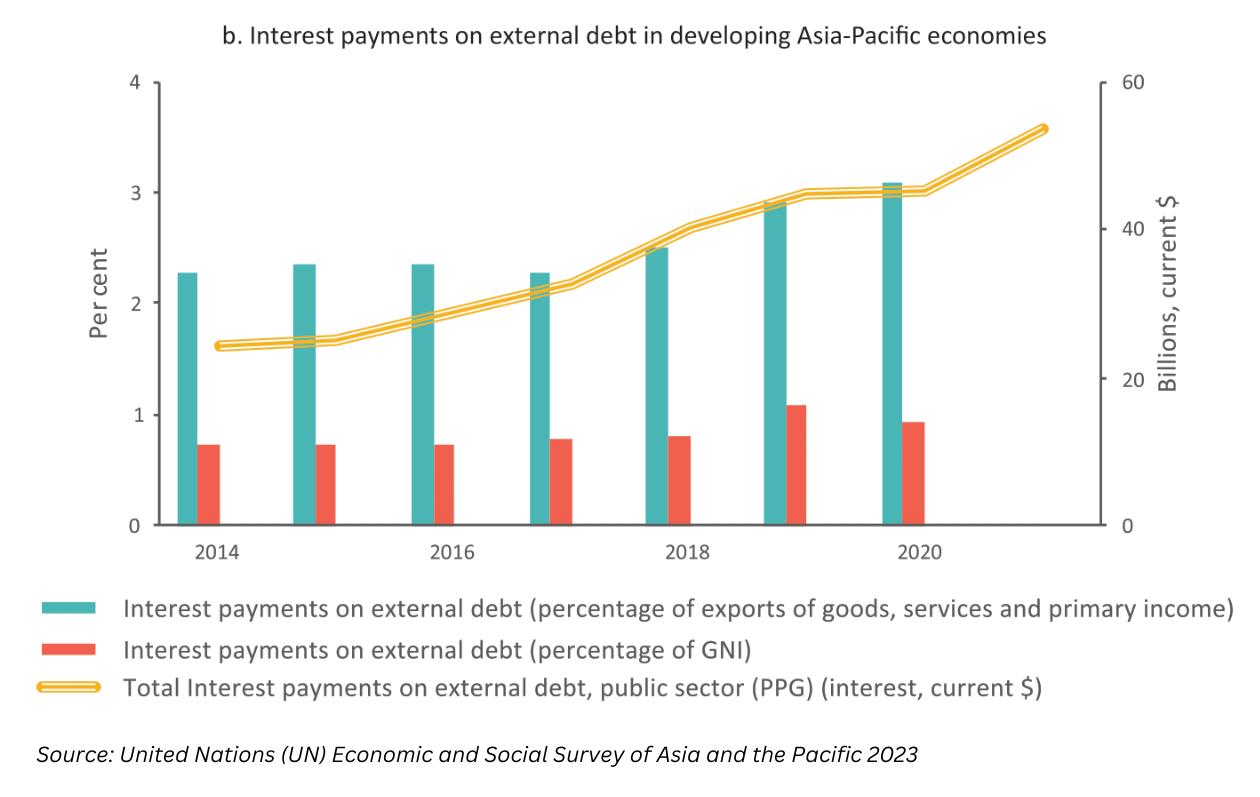

The report also highlighted that the current higher interest rate environment will raise debt servicing costs for governments, firms and households, and limit public and private investments.

“For economies with high household debt (Malaysia, South Korea and Thailand), there may be an impact on poverty as well,” it added.

The report noted that by the end of 2022, of 26 developing Asia-Pacific economies for which policy interest rate data is available, 22 had raised interest rates by an average of more than 300 basis points.

It said because there is a lag of nine to 12 months between a change in the monetary policy stance and its impact on inflation, central banks will have to wait until at least the middle of 2023 to start seeing some decline in inflation.

In focusing on the Asia-Pacific region, the report cited Pham (2018) empirical evidence of a significant and positive impact of public debt on real gross domestic product growth in six Asean countries during the period of 1995 to 2015, specifically in Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam.

Credit:Source link

{kind=link}